Many new expenses are being reported and mismatches can be a hassle. Updated returns can be filed within 24 months of the end of an assessment year

Many new expenses are being reported and mismatches can be a hassle. Updated returns can be filed within 24 months of the end of an assessment year

Navi Mumbai-based Rita Chatterjee, 63, a housewife, was stumped to see a message from the income tax department pointing at some high-value transactions reported under her Permanent Account Number (PAN). The message urged her to visit the compliance portal if she hadn’t yet filed her income-tax returns. In this instance, high-value transactions refer to tax deduction at source (TDS) transactions involving a sum of at least Rs 57,000 reported by banks.

Chatterjee wasn’t the only one to receive such a message. Various chartered accountants Moneycontrol reached out to over the last month have confirmed that hundreds of messages have been sent through SMS to Indian and non-resident Indians since March 2022.

These were pre-intimations triggered by the systems of the income tax department. “During the data-capturing exercise from various sources, if an income has been reported under your PAN and equivalent or matching data hasn’t been reported in your return then you would receive such triggers to file or revise returns,” a senior tax official told Moneycontrol, requesting anonymity.

There are at least 50 types of high-value transactions that get reported under the Annual Information Statement (AIS). The AIS is a financial summary of the taxpayer that is available with the income tax department and facilitates easy filing of tax returns. Information about various financial transactions executed by the taxpayer is obtained by the department from various financial entities (e.g., banks, stockbroking firms) that are delegated with the task of furnishing such information.

The AIS also includes details of your salary, rent, lottery wins, bank deposit interest, dividends above Rs 5,000, hotel bills above Rs 30,000, school fees and electricity bills above Rs 1 lakh, capital gains from offshore funds, foreign or Indian bonds, sale of land or vehicles, cash deposit and credit card bills above Rs 10 lakh, wherever TDS is paid by you.

Lately, earnings from virtual digital assets or cryptocurrencies and even gifts above Rs 20,000 are being reported.

What can you do?

Instead of panicking, check the pre-intimation. “Chances are that the transactions have been reported twice in the case of joint holders of mutual funds and bank accounts, and even though the second (joint) holder is not required to file a return, the message has been triggered,” says Paras Savla, partner at KBP & Associates.

When a notice is issued, you can respond by filing a return within the time limit mentioned in the notice. In this case, however, the messages are pre-emptive and aimed at nudging you to take action.

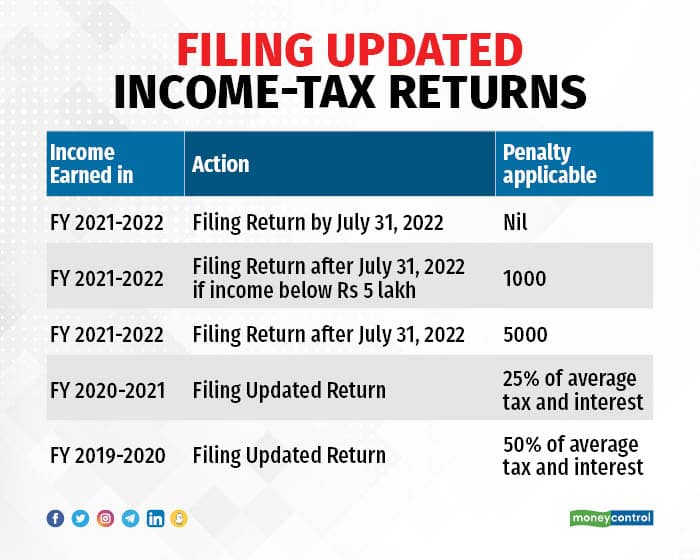

If this was for any other year, you would not have had the option of revising a return or filing a fresh return. For instance, income earned in financial year 2020-21 had to be reported by December 31, 2021 (extended deadline for the return) without any penalty. Even after the deadline, you could have filed your return by March 31, 2022, paying penal charges of Rs 1,000-5000.

A new provision for updated returns

However, in Union Budget 2022, a proposal was made to allow people to file updated returns by paying additional tax for up to two years from the end of the assessment year in which the income should have been accounted for.

“Per the newly introduced Section 139(8A) in the Income Tax Act, 1961, any person, whether or not he has filed a return, may furnish an updated return of his income — or the income of any other person in respect of which he is assessable under the IT Act — within 24 months from the end of the assessment year,” says Dr Suresh Surana, founder of RSM India.

So, if you filed a return on December 31, 2021, then the assessment year ends on March 31, 2022, and you can file the updated return under section 139(8A) till March 31, 2024. The updated return for the assessment year 2020-21, too, can be filed up to March 31, 2023.

Fresh returns can also be filed

Those who did not file a return in the past year and are now being subjected to double TDS deduction for non-filing can file a fresh return under the updated returns facility.

“The assessee can file the updated return with respect to any Original Return, Belated return, Revised Return or even file a fresh return,” says Surana.

Also, more people have been brought under the ambit of tax filing through a notification issued on April 22, 2022. Earlier only those with an income above the basic exemption limit of Rs 2.5 lakh (New Tax Regime) to Rs 5 lakh (Existing regime individuals and senior citizens) had to file an income tax return.

Now, individuals whose total tax deducted or collected at source exceeds Rs 25,000 (Rs 50,000 for senior citizens) during the financial year have to mandatorily file a tax return, even if their gross total income is below the basic exemption limit.

Additionally, those depositing Rs 50 lakh or more in savings bank accounts and Rs 1 crore or more in a current account, paying an electricity bill of Rs 1 lakh or more and spending Rs 2 lakh or more travelling to a foreign country have to file a tax return.

If your return has been filed, the compliance tracker will remove your PAN from the list of non-filers and you will not have to pay double the TDS.

Opportunity to declare Crypto assets

The regulations around virtual digital assets were announced in February 2022. Prior to that many individuals had either declared profits from crypto currencies as business gains or even capital gains. Others did not mention them in tax returns filed prior to December 31, 2021.

Individuals who want to come clean on crypto assets can use the updated return facility. “Those who haven’t declared their virtual assets in the return forms for the assessment year 2021-22 — as there was no clarity prior to Budget 2022 — can do so via the facility of an updated return,” says Savla.

He suggests that it is better to declare these during the assessment year 2022-23, using the updated return facility. “The rates are steeper at 50 percent if you declare these in the following year, which is two years after the assessment year when the income was earned, i.e. 2023-24,” Savla adds.

But crypto assets held long ago will not be permitted. “Updated returns can be filed by assessees only for the assessment year 2020-21 (FY 2019-20) and subsequent years,” says Surana.

Additional tax applicable

The tax applicable on updated returns is 25 percent if the return is filed within one year from the end of the assessment year. If the updated return is filed 12-24 months from the end of the assessment year, then tax will be applicable at 50 percent. The additional tax calculation would include cess and a surcharge on the base tax.

What you can’t declare

If you want to claim a refund or increase the quantum of your refund, then you cannot update the return. Also, if your return has been selected for re-assessment then you will not be able to update the return for that assessment year.

“Losses that you have incurred cannot be set off against income in an updated return. So, those who have not filed a return and want to declare losses lose out on the benefit,” says Savla.

You cannot reduce income by adjusting the loss carried forward under Chapter VI or unabsorbed depreciation carried forward under Section 32 (2).

Also, fill the updated return carefully. “No revision of an Updated Return is possible,” warns Surana.

Source: https://www.moneycontrol.com/news/business/personal-finance/couldnt-file-a-belated-income-tax-return-you-can-now-use-the-updated-tax-return-facility-8780391.html

© 2018 CA Chandan Agarwal. All rights reserved.