There is not much time left to file your taxes. This also means that you must choose your tax-saving investments in a huff if there are none.

There is not much time left to file your taxes. This also means that you must choose your tax-saving investments in a huff if there are none.

We plan our investments so meticulously, yet so many of us bungle up while planning our tax-saving investment options. A penny saved is a penny earned, thus, highlighting the need to focus on putting our money in investments that can help save on taxes too. If you are planning your tax-saving investments at the last minute, you must be well aware of how much you can invest and your risk profile apart from the estimated returns you are looking for.

To start with, you may check how much money is allocated to the Employees’ Provident Fund (EPF) account. Then, check if you recently bought any life insurance policies or are paying equated monthly instalments (EMIs) towards any home loan sought. This is because you can claim a deduction of up to ₹1.5 lakhs under Section 80C of the Income Tax Act, 1961.

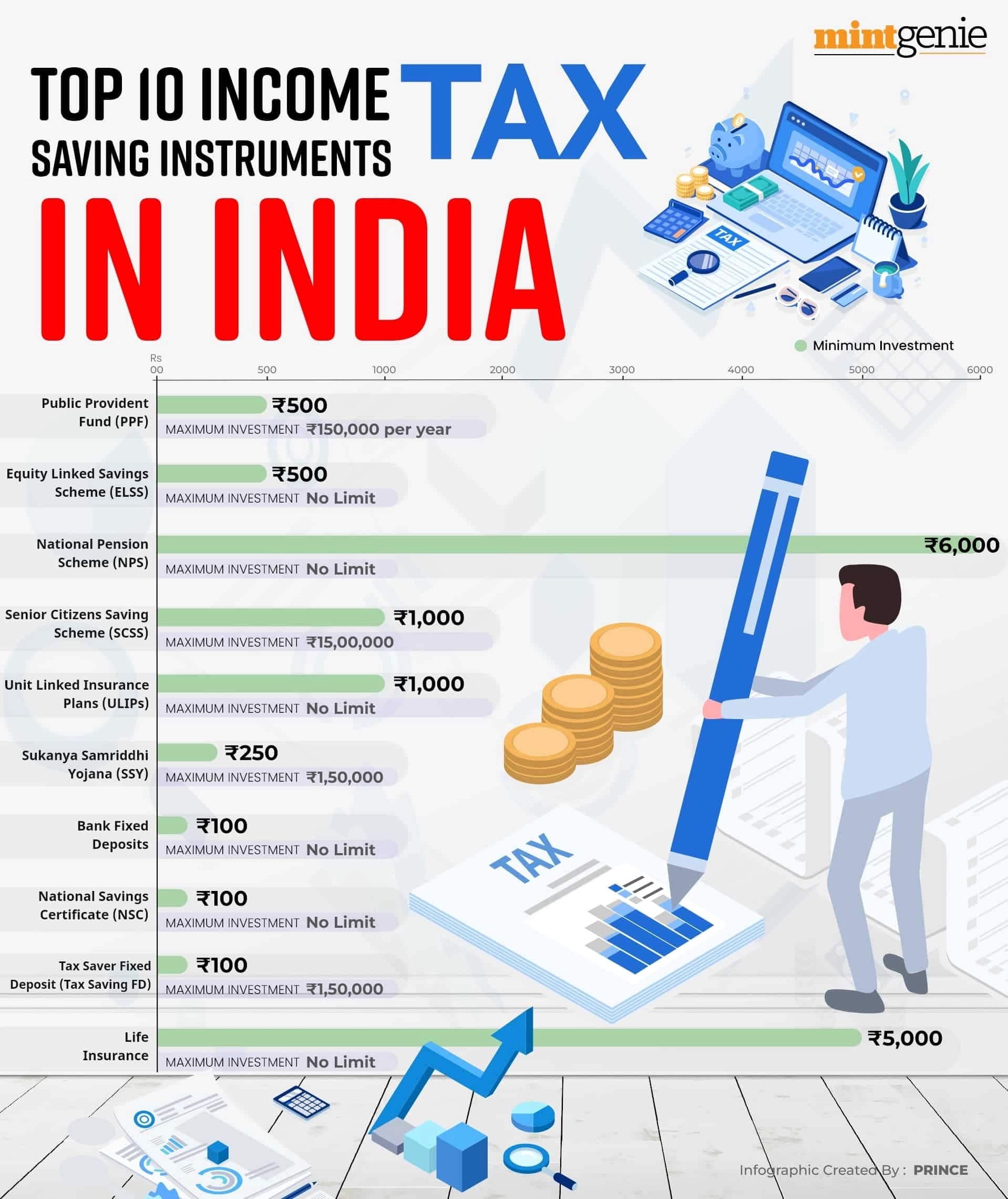

If you are aware of how much you wish to invest, you may start looking at the available investment options that not only avail you of good returns, thus, helping you create a corpus but also help on saving taxes too. Though there are many tax-saving options, only some are worthwhile when considered for last-minute tax-saving investments. These include:

Those willing to stay invested for at least 15 years can benefit from this small savings plan. The investment tenure is no doubt long though one may consider it to gain from the compounding effect on investments over the period. Moreover, it is a government-backed scheme that benefits from an exempt-exempt-exempt tax break. The amount invested, interest earned, and maturity withdrawals are all tax-free.

| Invested Amount (in Rs) | Total Interest (in Rs) | Maturity Value (in Rs) |

| 22,50,000 | 18,18,209 | 40,68,209 |

Apart, this is a risk-free investment option, thus, prompting many investors to put their earnings regularly in this fund. One may choose to invest monthly, quarterly, half-yearly or annually in this fund depending on their earnings and ability to garner the much-needed money to invest in this fund.

This is best suited for conservative investors who are looking to accumulate some money in the long run apart from saving on taxes under Section 80C of the Act. Unlike market-linked investments, where there is a risk on the capital amount invested, these bond-like instruments guarantee both interest and capital protection.

These certificates earn an annual fixed interest that is reviewed by the government every quarter, thus, ensuring a consistent income for the investor. The NSC interest rate for the period of January – March 2023 is seven per cent.

Investors may opt for the five-year bonds or the 10-year bonds depending on how they look at their finances. The best thing about these investments is that you can invest as low as ₹100 while there is no upper limit to these investments.

As evident from its name, this is a kind of investment option that puts money in equities and equity-linked instruments. This is the only kind of mutual fund scheme that also allows you to benefit from tax deductions under Section 80C of the Act. This means that investors can not only claim tax exemption up to ₹1,50,000 and save up to ₹46,800 in taxes every year by investing in this kind of fund.

The idea behind investing in this kind of scheme is to generate income and long-term capital appreciation from a diversified portfolio of predominantly equity and equity-related instruments. However, not all ELSS funds allocate the money to equities alone. Some invest only 60-65 per cent in equities while the remaining money is put in fixed-income securities.

Though these funds come with a lock-in period of three years, it makes sense to stay invested in them for a prolonged period, say a decade or more.

| Name of the ELSS fund | Three-year returns (in %) | Five-year returns (in %) | 10-year returns (in %) |

| Quant Tax Plan | 50.40 | 22.17 | 22.32 |

| Bandhan Tax Advantage (ELSS) Fund | 36.78 | 12.84 | 17.89 |

| Kotak Tax Saver Fund | 28.60 | 14.28 | 16.19 |

| Sundaram Tax Saving Fund | 27.36 | 9.83 | 15.75 |

| Canara Robeco Equity Tax Saver Fund | 27.43 | 15.44 | 15.72 |

| Franklin India Taxshield Fund | 29.05 | 11.26 | 15.21 |

| Source: MoneyControl | |||

Medical costs are going up with an increase in expenses on both hospitalization and subsequent treatment. Treatment is costly as effective, which means that one has to spend more to ensure adequate treatment. Post-hospitalization treatment can also be costly, which means that one must have enough savings to pay for the same.

Alternatively, you may also buy a health insurance plan that allows you to seek exemption up to ₹100,000 on premiums under Section 80D of the Act. This means that you may seek exemption up to ₹50,000 on premiums paid towards health insurance bought for yourself and your family and ₹50,000 on premiums for health policies bought for senior citizen parents.

These investment options are appropriate for seniors as well as risk-averse investors. Individuals can claim a tax deduction under Section 80C for investing in five-year tax-saving fixed deposits (FDs). This is one of the most sought-after options that not only help to save adequately but also contribute to overall tax savings.

If you are looking to save on taxes beyond what is stipulated under Section 80C of the Act, you may consider putting your earnings in the National Pension Scheme (NPS). This is a government-sponsored scheme initially opened for government employees but was later opened to all. This is a retirement savings plan designed to help subscribers make the best decisions for their future by making systematic savings throughout their working lives.

The NPS aims to instil in citizens the habit of saving for retirement. It is an attempt to find a long-term solution to the problem of providing adequate retirement income to every Indian citizen. Section 80CCD of the Income Tax Act governs the deductions available to people who make NPS contributions, thus, allowing an added tax deduction of ₹50,000 under the scheme.

Tax-saving options are myriad and plenty, thus, allowing investors to choose according to their risk appetite and financial goals. This allows them to choose from various insurance plans, mutual funds and government-sponsored schemes. However, the tendency to invest in tax-saving options disallows investors to weigh the pros and cons of every investment before deciding to put their money in them.

Source: https://mintgenie.livemint.com/news/personal-finance/looking-for-income-tax-saving-options-at-the-last-moment-here-s-what-you-can-consider-151679407211165

© 2018 CA Chandan Agarwal. All rights reserved.