Opted for new tax regime? Here’s a list of deductions you can consider

- March 25, 2024

- CA Chandan Agarwal's Office

As the financial year draws to a close on March 31, taxpayers are exploring avenues to optimise their financial strategies and minimise tax liabilities under the new tax regime. Here’s a comparative list of deductions under the old and new tax regimes to help you make the right choices.

As the financial year draws to a close on March 31, taxpayers are exploring avenues to optimise their financial strategies and minimise tax liabilities under the new tax regime. Here’s a comparative list of deductions under the old and new tax regimes to help you make the right choices.

As the end of the financial year 2023-24 approaches, investors must be seeking avenues to minimise their tax burden and increase savings. Given the availability of two income tax regime options, it’s likely that certain taxpayers have opted for the new regime, characterised by lower tax rates albeit fewer deductions.

Introduced under Section 115BAC in Budget 2020, the new tax regime has now become a default option. If you do not opt for either regime, the new one will be automatically selected.

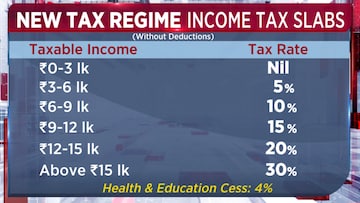

A look at new tax regime rates

Individuals with an annual income up to ₹3 lakh are not liable to pay any tax under the new tax regime.

A 5% tax rate is applicable for those with an income between ₹3-6 lakh, 10% for an income between ₹6-9 lakh, 15% for an income between ₹9-12 lakh, 20% for an income between ₹12-15 lakh, and 30% for income above ₹15 lakh.

It’s important to note that a tax rebate is currently available on income up to ₹7 lakh, potentially benefiting those with salaries up to ₹7.5 lakh.

Allowances and deductions available

A standard deduction of ₹50,000 is available to all taxpayers, irrespective of income level.

Taxpayers can also avail deduction on long-term capital gains from the sale of equity shares or equity-oriented mutual funds, up to ₹1 lakh.

Additionally, tax exemptions are available for various allowances such as transport, conveyance, travel, perquisites for official purposes, exemptions for voluntary retirement scheme, leave encashment, interest on home loan on lent-out property, gifts of up to ₹5,000, employer’s contributions to employees NPS accounts, among others.

What’s not allowed under the new regime

Deductions under Chapter VIA, including Section 80C, 80D (premium on health insurance), and 80E, except for Section 80CCD(2) and Section 80JJAA, are not permitted under the new tax regime.

Comparison of deductions under old regime vs new regime

| Available Exemptions/ Deductions |

Old Tax Regime |

New Tax Regime |

| Standard Deductions of Rs. 50,000 u/ Section 80TTB Deduction |

YES |

YES |

| Employment/ Professional Tax u/ Sec 10(5) |

YES |

NO |

| House Rent Allowance (HRA) u/ Sec 10(13A) |

YES |

NO |

| Exemptions for Free Food & Beverages through Vouchers/ Food Coupons |

YES |

NO |

| Deductions of up to ₹1.5 lakhs u/ Chapter VIA towards investments like u/ Sec 80C, 80CCC, 80CCD, 80DD, 80DDB, 80E, 80EE, 80EEA, 80G, etc. |

YES |

NO |

| Deductions u/ Sec 80CCD(2) for Employer’s Contribution to Employee NPS Accounts |

YES |

YES |

| Deductions u/Sec 80CCD(1B) of Up to ₹50,000 |

YES |

NO |

| Medical Insurance Premium u/Sec 80D |

YES |

NO |

| Interest on Home Loan for Self-Occupied/ Vacant Property |

YES |

NO |

Source: https://www.cnbctv18.com/personal-finance/income-tax-regime-new-vs-old-list-of-deductions-available-investment-savings-home-loan-19346761.htm